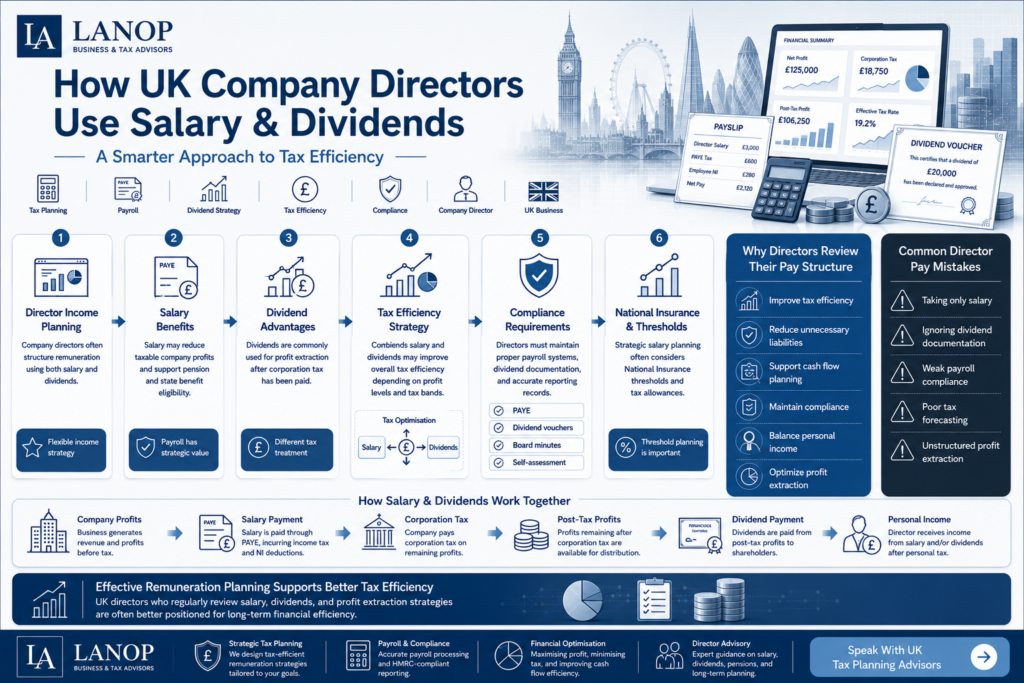

Director Salary and Dividends: The Most Tax-Efficient Setup for UK Companies

Most directors running their own limited company ask the same question eventually. Not “how do I grow revenue” or “when should I hire” but “what is the smartest way to actually pay myself?”

It sounds straightforward. Take a small salary, draw the rest as dividends, pay less tax. That’s the advice you’ll hear at networking events, read on forums, and pick up from well-meaning peers. The problem is that it’s incomplete and for many directors, following it blindly costs real money. Finding a good accountant for limited company directors is often what separates those who genuinely optimise their take-home pay from those who think they are.

This guide walks through how director remuneration actually works, where the common strategies fall short, and how to think about your own setup more clearly.

Why Getting This Wrong Is More Expensive Than You Think?

Before getting into strategy, it’s worth understanding what’s actually at stake.

Directors who pay themselves inefficiently don’t just overpay tax they often lose National Insurance credits that affect their State Pension entitlement, reduce their mortgage borrowing power by structuring income in ways lenders don’t like, and miss pension planning opportunities that could shelter significant sums from tax entirely. None of these consequences show up immediately. They accumulate quietly over years, which is exactly why so many directors don’t notice until the damage is done.

The “low salary, high dividend” approach isn’t wrong in principle. It’s just not universally correct and the gap between those two things matters enormously depending on your profit level, personal circumstances, and what you’re trying to achieve financially.

Three Ways Directors Actually Take Money Out

Understanding your options clearly is the foundation of any sensible remuneration strategy.

Salary through PAYE works exactly as it does for any employee. The company pays you, deducts Income Tax and National Insurance, and reports everything to HMRC. Salary is a business expense, which means it reduces the company’s taxable profit before Corporation Tax applies. That’s a meaningful point that often gets lost in conversations focused purely on personal tax rates.

Dividends come from company profits after Corporation Tax. You can only pay dividends if the company has sufficient distributable profits not just cash in the bank, but actual recorded profit after all liabilities. Dividends don’t attract National Insurance, which is the core reason they’re tax-efficient. They do attract Dividend Tax, currently charged at 8.75% for basic rate taxpayers, 33.75% at higher rate, and 39.35% at additional rate but even at higher rates, this usually beats the equivalent Income Tax and NI combination.

Director’s loan accounts sit in a different category entirely. When a director takes money from the company that isn’t salary or dividends, it goes through the loan account. This can be useful for short-term cash flow, but mismanaging it creates serious tax problems. Overdrawn loan accounts above £10,000 trigger a benefit-in-kind charge. If the loan isn’t repaid within nine months of the company’s accounting year-end, the company faces a 33.75% Corporation Tax charge on the outstanding balance under S455. It’s a trap that catches more directors than you’d expect.

What the Comparison Actually Looks Like?(Salary vs Dividends)

People often frame this as a binary choice. In practice, the question is never “salary or dividends”, it’s always “how much of each, and when.”

Salary gives you pensionable income, NI credits, and a clean paper trail that mortgage lenders understand. Dividends give you lower tax rates, more flexibility on timing, and no NI liability. Pension contributions sit alongside both and deserve more attention than most directors give them.

The key tension comes down to this: salary reduces Corporation Tax but attracts Income Tax and NI. Dividends come from already-taxed profit but carry lower personal tax rates. At first glance, paying Corporation Tax then Dividend Tax sounds inefficient compared to just taking salary. Run the actual numbers and the picture changes.

Take a director extracting £50,000 from a company. A £50,000 salary costs the company nothing extra in Corporation Tax but the director pays Income Tax at 20-40% plus National Insurance. Draw the same amount through a modest salary and dividends, and the combined tax burden across both the company and the director typically comes out lower. The combined rate advantage of dividends usually persists even after Corporation Tax, particularly for basic and higher rate taxpayers.

What Is the Most Tax-Efficient Director Salary?

This is the question most directors get partially right and the details matter.

The optimal salary figure sits around the National Insurance Secondary Threshold, currently £9,100 per year, or sometimes up to the Primary Threshold of £12,570 where the personal allowance ends. The exact sweet spot depends on whether the company can claim the Employment Allowance, which offsets employer NI up to £5,000 annually.

For a sole director company that cannot claim the Employment Allowance, setting salary at £9,100 avoids both employee and employer NI while still generating a qualifying year for State Pension purposes. For companies with other employees where the allowance applies, a salary up to £12,570 often makes more sense; the personal allowance absorbs the Income Tax liability, and the employer NI gets covered by the allowance.

Taking no salary at all carries its own risk. Without a qualifying salary, directors don’t accumulate NI credits for the year, which affects State Pension entitlement over time. Thirty-five qualifying years are needed for a full State Pension. For a director in their 40s, missing even five or six years adds up.

How Profit Level Changes Everything?

The right remuneration strategy at £30,000 profit looks nothing like the right strategy at £150,000.

At £30,000 company profit, there isn’t much room to manoeuvre. After a modest salary and Corporation Tax, the remaining distributable profit might be £18,000–£20,000. The dividend allowance (currently £500) covers a small portion tax-free, and the rest falls within the basic rate band. The overall tax position is reasonable, but the savings over a sole trader at this level are often modest once accountancy costs are factored in.

At £50,000–£75,000 profit, the strategy starts delivering meaningfully. A salary around the NI threshold, dividends extracted up to the higher rate threshold, and potentially some pension contributions to reduce the company’s taxable profit can produce a noticeably better outcome than salary alone. Directors in this range often see effective personal tax rates well below what an equivalent employed salary would attract.

At £100,000 and above, more sophisticated planning becomes genuinely worthwhile. Pension contributions through the company become powerful; they reduce Corporation Tax and avoid the personal allowance taper that kicks in above £100,000. Leaving some profit inside the company rather than extracting everything annually can smooth income across years and manage personal tax bands more effectively. Husband-and-wife or family-owned structures open up income-splitting opportunities that can reduce the household tax burden further, provided shareholdings and dividend payments are commercially justified and properly documented.

The Problem Nobody Warns You About(Dividends and Mortgages)

Here’s a real-world consequence that catches directors off guard.

Many mortgage lenders don’t assess director income the same way they assess employed income. Some lenders use salary only. Others use salary plus dividends. A smaller number will consider retained profits inside the company. The variation is significant and choosing a remuneration strategy purely for tax efficiency, without thinking about mortgage implications, can leave you unable to borrow what you need when you actually need it.

A director taking £9,100 salary and £40,000 in dividends may have a total personal income of just over £49,000 but a lender using salary multiples only sees £9,100. That’s not a mortgage, that’s a problem. The solution isn’t to abandon the dividend strategy, but to plan remuneration with a specialist who understands both the tax and lending implications together.

Paying Dividends Correctly: The Steps Most Directors Skip

Dividends aren’t just transfers from the company account to your personal account. They require proper process, and HMRC does scrutinise this.

The company must have sufficient distributable profits retained earnings after Corporation Tax, as shown in the accounts. A director can’t pay dividends based on cash in the bank if the profit isn’t there on paper. Beyond that, dividends require a board resolution (even if you’re the sole director), and each payment needs a dividend voucher documenting the date, amount per share, and total payment. These aren’t bureaucratic formalities, they’re the difference between a legitimate dividend and an illegal one.

Illegal dividends, paid without sufficient profits, don’t disappear. HMRC can reclassify them as salary, triggering Income Tax and National Insurance on the full amount plus interest and penalties. The documentation requirement exists to protect directors as much as it protects HMRC.

The Underused Tool(Pension Contributions)

Most directors focus on the salary-dividend split and stop there. Pension contributions deserve equal attention particularly for higher earners.

Company pension contributions are a business expense. They reduce the company’s profit before Corporation Tax applies, effectively giving the company tax relief at 25% on every pound contributed. The money goes into the director’s pension rather than being taxed twice through Corporation Tax and then Dividend Tax. For a director in their 40s or 50s with meaningful profits, this can be one of the most efficient ways to extract value from the company.

The annual pension allowance currently £60,000 sets the ceiling for tax-relievable contributions. Unused allowance from previous years can be carried forward under certain conditions, creating planning opportunities for directors who haven’t used pensions strategically until now.

Common Mistakes Worth Avoiding

A few patterns come up repeatedly among directors who manage remuneration without proper advice. Any experienced accountant for limited company directors will tell you the same mistakes surface again and again and most of them are entirely avoidable with the right guidance.

Taking dividends without checking the profit position is probably the most common. Cash in the account feels like profit but if the retained earnings aren’t there to support the dividend, the payment is illegal regardless of how much cash sits in the bank.

Ignoring pension contributions is the second. The tax arithmetic is compelling, particularly above the basic rate threshold, and most directors who start using company pensions seriously wish they’d done it earlier.

Mixing company and personal finances through casual use of the director’s loan account is the third. A few unexplained transfers can create a compliance headache that takes an accountant several hours to unravel and costs considerably more than it would have to keep things clean from the start.

Frequently Asked Questions

Can I take only dividends and no salary as a director?

Technically yes, but it’s not advisable. Taking no salary means losing National Insurance credits that count toward your State Pension. A small salary set around the NI threshold costs you nothing in actual NI liability but keeps your pension record intact. Dividend-only looks efficient short-term but creates an expensive gap long-term.

How often can I pay myself dividends?

As often as the company has sufficient distributable profit monthly, quarterly, or annually. Frequency isn’t the issue. Every payment needs a board resolution and dividend voucher regardless. Directors who skip the paperwork and treat informal transfers as dividends after the fact invite HMRC scrutiny.

Do dividends count toward my mortgage application?

It depends on the lender. Some accept salary plus dividends, others use salary only. A director earning £9,100 salary and £45,000 in dividends has a combined income of £54,000 but certain lenders only see £9,100. Always speak to a broker who understands limited company director income before restructuring your remuneration.

What happens if my company pays a dividend without enough profit?

HMRC can reclassify it as salary, triggering Income Tax and National Insurance on the full amount plus interest and penalties. Cash in the bank doesn’t make a dividend legal. Distributable reserves recorded in the accounts do. Always check the profit position before declaring any payment.

Are pension contributions more tax-efficient than dividends?

Often yes, particularly for higher earners. Company pension contributions reduce profit before Corporation Tax applies, bypassing Dividend Tax entirely. Extracting the same amount as a dividend means paying Corporation Tax first, then Dividend Tax on what remains. For directors above the basic rate threshold, the pension route frequently wins.

Conclusion

Salary and dividends aren’t a formula to apply once and forget. The optimal mix shifts as profit grows, tax rules change, and personal circumstances evolve. What worked at £60,000 profit may not serve you at £120,000.

That’s where Lanop Business & Tax Advisors comes in. Lanop works with directors year-round adjusting salary and dividend splits, identifying pension opportunities, and making sure your strategy reflects where your business actually stands today.

If your remuneration hasn’t been reviewed recently, speaking with a qualified corporate tax accountant at Lanop is the smartest next step. The savings usually speak for themselves.